|

|

|

|---|

|

|

|

|---|---|---|

|

|

|

|

|

|

|---|---|---|

|

|

|

|

Comprehensive Guide on Filing Bankruptcy: Key Steps and Considerations

Filing for bankruptcy can be a challenging decision. Understanding the process and knowing the common pitfalls to avoid can make it more manageable. This guide aims to provide essential information on filing bankruptcy, helping you navigate through this complex process.

Understanding Bankruptcy

Bankruptcy is a legal process designed to help individuals or businesses eliminate or repay their debts under the protection of the bankruptcy court. It's crucial to understand the types of bankruptcy before proceeding.

Types of Bankruptcy

There are several types of bankruptcy, but the most common for individuals are Chapter 7 and Chapter 13.

- Chapter 7: Known as liquidation bankruptcy, this type involves selling non-exempt assets to pay off creditors.

- Chapter 13: This is a reorganization bankruptcy where you create a repayment plan to pay back all or part of your debts over three to five years.

Steps to File for Bankruptcy

- Gather Financial Documents: Collect all relevant financial documents such as income records, asset lists, and debt statements.

- Credit Counseling: Complete a credit counseling course from an approved agency. This is a mandatory step before filing.

- File the Petition: Submit the bankruptcy petition, including all required schedules, to the bankruptcy court.

- Meet the Trustee: Attend a meeting with your appointed trustee to review your case.

- Complete Debtor Education: Attend a debtor education course before your debts can be discharged.

Common Mistakes to Avoid

Filing for bankruptcy involves several pitfalls. Avoiding these can lead to a smoother process and better outcomes.

- Failure to Disclose All Assets: Not listing all your assets can lead to your case being dismissed.

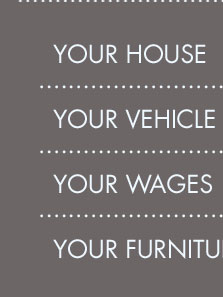

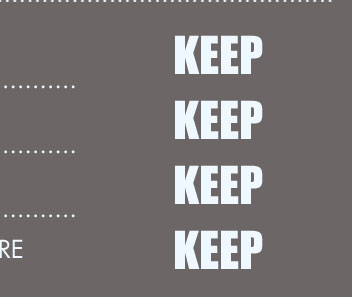

- Ignoring Exemptions: Properly claiming exemptions can help you retain essential assets.

- Last-Minute Spending: Making large purchases before filing can be considered fraudulent and harm your case.

For more personalized advice, consider consulting with bankruptcy indiana lawyers who are well-versed in local laws and regulations.

After Filing for Bankruptcy

Life after bankruptcy can be challenging, but with careful planning, you can rebuild your financial health.

- Build a Budget: Create a realistic budget to manage your finances post-bankruptcy.

- Rebuild Credit: Start rebuilding your credit by paying bills on time and using credit responsibly.

For additional resources, the bankruptcy law center portland or offers comprehensive support and guidance.

Frequently Asked Questions

What is the difference between Chapter 7 and Chapter 13 bankruptcy?

Chapter 7 involves liquidating assets to repay debts, while Chapter 13 allows for a repayment plan over time. The choice depends on your financial situation and goals.

How long does bankruptcy stay on my credit report?

A Chapter 7 bankruptcy can remain on your credit report for up to 10 years, while a Chapter 13 can stay for up to 7 years. It's important to work on rebuilding credit during this period.

The debtor files papers with the U.S. Bankruptcy Court (which is a federal court). By filing these papers, debtors are telling all creditors ( ...

Filing decisions and prebankruptcy planning. Gathering documents and completing the forms. Filing information specific to your state.

Some taxes may be dischargeable. Whether a federal tax debt may be discharged depends on the unique facts and circumstances of each case.

![]()

![]()